Algorithmic Markets: How AI and Automation Are Shaking Up Higher Education and Economic Theory

The global financial ecosystem is undergoing a silent, systemic mutation. Over the past decade, high-frequency trading (HFT) platforms, predictive neural networks, and automated liquidity protocols have decoupled modern financial operations from human emotional biases. By 2026, algorithmic execution systems are estimated to govern upwards of 80% of daily US equity trade volumes. This structural transformation extends far beyond the quantitative trading desks of Wall Street; it is violently rippling backward into academia, rewriting core tenets of economic modeling, and challenging foundational instructional methods within higher education across the United States.

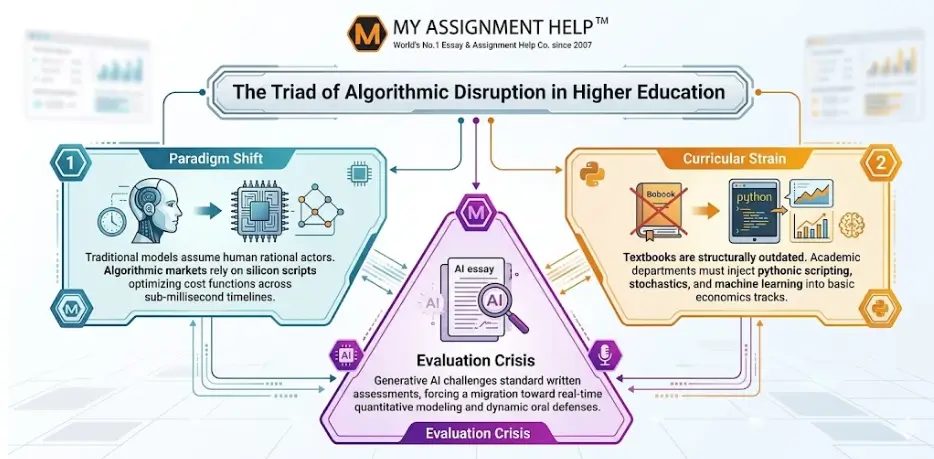

For decades, traditional macroeconomic and microeconomic models operated under the convenient fiction of the Homo economicus—the perfectly rational agent acting in clear self-interest based on readily available, symmetric market signals. Today, however, autonomous software scripts execute hyper-complex arbitrage strategies within fractions of a microsecond, processing multi-structured datasets that no human mind could synthesize in a lifetime. As traditional theoretical frameworks buckle under the pressure of these artificial realities, American universities are encountering an urgent pedagogical crisis: how to educate a new generation of analysts when textbook definitions of market efficiency, consumer equilibrium, and price discovery have become obsolete artifacts of a pre-algorithmic era.

The Evolution of Economic Agents: From Rational Minds to Silicon Scripts

Classic economic theory relies heavily on the concept of rational expectations. In this paradigm, agents use all available information to form expectations about future economic variables, ensuring that systematic forecasting errors are neutralized over time. Yet, when the predominant market participants shift from human portfolio managers to deep reinforcement learning agents, the operational mechanics of decision-making undergo an epochal shift. Algorithmic agents do not evaluate utility curves through qualitative assessments of market sentiment; they optimize objective cost functions by continuously executing trillions of stochastic simulations.

Consider the classic formula for market price adjustment under standard competitive equilibrium assumptions. Traditionally, price changes (\Delta P) are modeled as a direct function of excess demand (D – S), expressed as:

\Delta P_t = \lambda(D_t – S_t) + \varepsilon_t

Where \lambda represents the speed of market adjustment and \varepsilon_t accounts for random white noise shocks. In an environment heavily dominated by automated algorithms, \lambda approaches infinity during localized intervals, compressed into millisecond horizons, while \varepsilon_t is no longer random noise but rather highly coordinated, endogenous algorithmic signals designed to trigger stop-loss thresholds of competing scripts. Consequently, the traditional mechanisms of price discovery break down entirely, leaving academic economists scrambling to formalize models that can account for sudden, cascading systemic collapses like “flash crashes”.

The Curricular Breakdown in US Higher Education

As academic researchers struggle to keep pace with algorithmic realities, undergraduate economics departments across the United States are grappling with a compounding structural misalignment. Standard educational paths typically divide economic training into qualitative theory and quantitative econometrics. However, this bifurcation fails in an age of automated high-frequency trading and large language model predictive analytics. Students routinely find that while they can calculate theoretical deadweight loss on a blackboard, they are completely illiterate when confronted with real-time algorithmic order books or non-linear predictive arrays.

Leading private and public institutions, from Boston to Berkeley, are rapidly adjusting their foundational requirements out of sheer necessity. Elite business schools are systematically retiring standard introductory macroeconomics courses to clear the way for interdisciplinary paths that blend computational data science, pythonic modeling, and machine learning stochastics. The demand for highly specialized quantitative literacy has reached unprecedented heights.

| Traditional Curriculum Model PDF+ 1 | Algorithmic / Modern Curriculum Model PDF+ 1 | Strategic Educational Focus PDF+ 1 |

| Static Supply & Demand Curves | Dynamic, High-Frequency Order Book Dynamics | Microstructural Liquidity Tracking |

| Linear Econometric Regressions (OLS) | Non-Linear Neural Networks & Random Forests | Predictive Structural Modeling |

| Homo Economicus Rational Agency | Multi-Agent Automated Reinforcement Systems | Behavioral Systemic Simulations |

| Qualitative Macro-Policy Summaries | Algorithmic Sentiment Analysis & NLP Processing | Real-Time Unstructured Data Processing |

Navigating Modern Scholastic Demands in Computational Fields

This sudden, macro-level operational shift places severe pressure on undergraduates struggling to master traditional text definitions while simultaneously configuring quantitative data code. Navigating these overlapping, multidisciplinary workloads successfully requires top-tier secondary research materials and data modeling workflows. When college students face compressed timelines or complex thesis formatting, securing professional essay writing help USA platforms ensures that structural organization and citation accuracy align directly with strict grading rubrics.

The evaluation process becomes significantly more complex when standard assignments involve calculating multi-agent predictive arrays or processing real-time market microstructures. For specialized upper-division coursework, general academic guidance is rarely sufficient to handle advanced econometric proofs. In these scenarios, collaborating with a seasoned economics essay writer allows students to bridge the gap between abstract algorithmic concepts and empirical data presentation, preserving their cumulative GPA while navigating computational program demands.

Generative AI and the Academic Integrity Redesign

The rise of automated trading algorithms is mirrored closely by the explosion of generative artificial intelligence inside the classroom. The deployment of advanced transformer models has fundamentally disrupted traditional evaluation mechanics. For nearly a century, the standard undergraduate evaluation vehicle was the take-home synthesis essay or the qualitative analytical report. Today, generative platforms can instantly produce superficially sound papers on standard topics, rendering old assessment methodologies obsolete.

This has driven US colleges into an intense re-evaluation of educational authenticity. Rather than relying on outdated automated detection platforms that suffer from high false-positive rates and systemic bias against non-native English speakers, forward-thinking university administrations are overhauling their grading metrics entirely. There is a strong movement back toward in-person synthesis labs, real-time algorithmic simulations, and interactive oral examinations. Academic leaders recognize that the goal is not to bar AI from student use, but to teach students to leverage automation ethically while demonstrating distinct, human-driven “Information Gain”—insights that transcend the baseline summaries found in generic training data.

Key Takeaways for Academic & Industry Leaders

- Theoretical Obsolescence: Traditional economic models based exclusively on slow-moving human rationality must be radically expanded to integrate multi-agent machine learning frameworks.

- Interdisciplinary Urgency: Economics departments must deeply embed advanced computer science, python scripting, and stochastic modeling directly into core undergraduate degrees.

- Assessment Revolution: The reliance on static, qualitative take-home essays is declining, replaced by dynamic, interactive simulations and oral defenses to ensure genuine critical evaluation.

- Ethical Coexistence: Success in the modern corporate landscape requires a symbiotic approach where human critical thinking guides automated tool deployment.

Reconceptualizing Market Microstructure and Financial Stability

The theoretical consequences of widespread market automation challenge the core assumptions of welfare economics. The first fundamental theorem of welfare economics states that competitive markets tend toward Pareto efficient allocations under specific conditions. However, this assumes that information transmission is costless and that agents do not possess asymmetrical computational advantages. In algorithmic markets, the entity with the lowest latency or the most advanced predictive model captures immediate economic rents, distorting resource allocation.

Furthermore, machine learning models running on continuous feedback loops often converge on unintended cooperative behaviors without explicit human direction. This phenomenon, known as algorithmic tacit collusion, occurs when pricing scripts independently discover that maintaining artificially high margins yields superior long-term returns compared to aggressive price competition. Regulators at the Federal Trade Commission (FTC) and academic theorists are realizing that old antitrust laws, developed to address physical cartels meeting in smoky backrooms, are entirely unequipped to police self-learning neural networks communicating through subtle order book manipulations.

Conclusion: The Future of Economic Literacy

The collision of algorithmic automation, modern financial markets, and the US higher education system is an irreversible evolutionary shift. As silicon scripts continue to displace human agency across global trading desks, the discipline of economics must adapt or risk total obsolescence. University classrooms can no longer remain isolated sanctuaries of 20th-century economic theory; they must transform into active experimental labs where quantitative computing, data science, and ethical synthesis converge seamlessly.

For the modern student, navigating this highly demanding educational environment requires intense dedication, intellectual agility, and a willingness to utilize advanced structural support mechanisms. By embracing this disruptive wave rather than resisting it, academia can cultivate a sophisticated class of financial strategists and economic thinkers who are fully prepared to govern, optimize, and ethically guide the highly automated market networks of tomorrow.

See also: The Role of Blockchain in Digital Identity

Frequently Asked Questions (FAQ)

Q1: What exactly is an algorithmic market?

A1: An algorithmic market is a financial environment where trading decisions, liquidity provision, and asset allocations are executed predominantly by automated computer programs using complex mathematical rules and machine learning algorithms, rather than by human traders.

Q2: Why are traditional economic models failing in modern financial landscapes?

A2: Traditional models assume that human actors operate with bounded rationality over extended intervals. They fail because automated scripts execute decisions at microsecond speeds, process non-linear data arrays, and exhibit automated emergent behaviors that traditional static models cannot predict.

Q3: How are American universities changing their economic curricula to adapt?

A3: Universities are introducing interdisciplinary degrees that merge advanced mathematics, python programming, and machine learning directly with economic theory, ensuring students learn to model algorithmic microstructures alongside standard macro policies.

Q4: How can students handle the rising quantitative difficulty in these programs?

A4: Students are increasingly utilizing highly specialized academic support tools and expert consultancies to clarify complex data-modeling concepts, build robust research frameworks, and maintain competitive GPA metrics.

Q5: What is algorithmic tacit collusion?

A5: It is a phenomenon where independent machine learning algorithms, optimizing for profit, naturally learn to avoid price wars and coordinate pricing structures dynamically without any explicit human interaction or illegal communication.

Author Biography

Dr. Marcus Vance holds a Ph.D. in Quantitative Economics from a premier US institution and acts as a Principal Academic Strategy Researcher at MyAssignmentHelp. With over twelve years of experience bridging the gap between algorithmic trading theory and academic pedagogical design, Dr. Vance focuses on developing advanced data literacy frameworks for contemporary higher education curriculums. He regularly publishes on macro-structural educational shifts and technological integrations in modern finance.